By Patrick Cheng, CEO eKare

2/9/2026

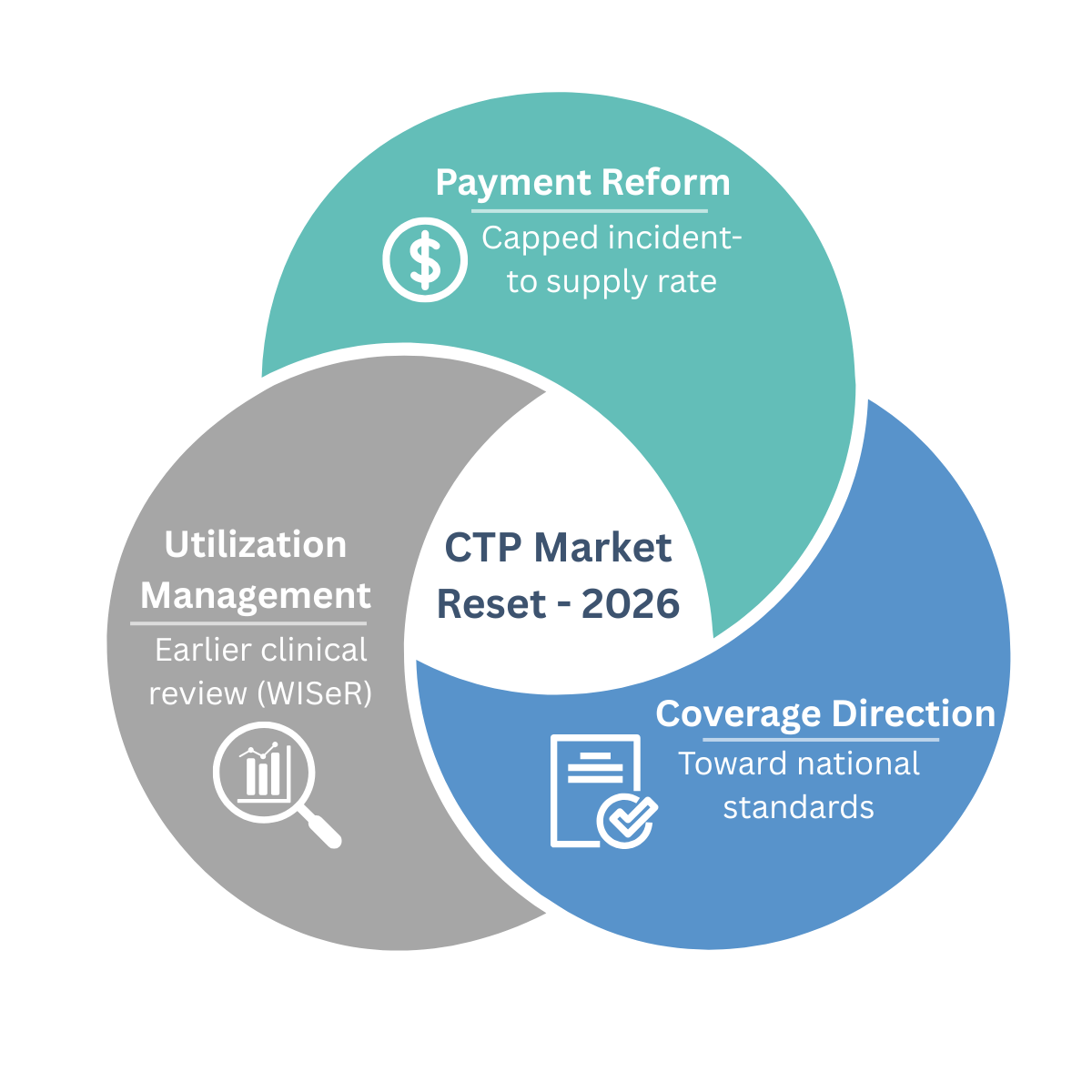

CMS isn’t taking a single swing at the CTP market. It’s using the whole toolkit.

Over the last several years, the cellular and tissue-based products (CTP) space has seen rapid growth in utilization and spend, paired with uneven product quality, inconsistent documentation, and a long tail of questionable billing patterns. That combination of runaway spend plus enforcement headlines has led to a predictable response: CMS deploying multiple, coordinated levers to curb fraud and abuse and tighten medical necessity.

The key takeaway for 2026 and beyond is simple: this is not about one policy document. It’s a system-level reset with clinical evidence at the center.

The 2026 Reset: Payment Changed Even Though LCDs Didn’t

1) A new payment ceiling

For CY 2026, CMS finalized a major shift in how most skin substitutes are paid moving from ASP-style reimbursement to an incident-to supply model with a single capped rate. CMS initially cited ~$127.28/cm², later corrected to $127.14/cm².

CMS estimates this change will reduce Medicare spending on these products by nearly 90%, projecting approximately $19.6B in reduced gross fee-for-service spending in 20261, while explicitly stating the policy is intended to “incentivize the use of products with the most clinical evidence of success.”

CMS estimates this change will reduce Medicare spending on these products by nearly 90%, projecting approximately $19.6B in reduced gross fee-for-service spending in 20261, while explicitly stating the policy is intended to “incentivize the use of products with the most clinical evidence of success.”

Practical impact: the economics of product selection are changing fast. In a capped-payment environment, clinical differentiation matters more than reimbursement spread.

2) The “national LCD” effort was pulled back but the direction didn’t change

In December 2025, CMS withdrew the DFU/VLU skin substitute LCDs that were set to take effect across all A/B MACs. Those harmonized LCDs would have functioned as a quasi-national coverage framework an approach that tends to draw scrutiny around evidence standards, process, and transparency.

With the withdrawal, the product-list-driven coverage change did not take effect. But this should not be interpreted as a return to business as usual. Payment reform moved forward, and coverage scrutiny did not disappear.

3) WISeR moves utilization management upstream

The WISeR (Wasteful and Inappropriate Service Reduction) Model launches January 1, 2026, across six states (NJ, OH, OK, TX, AZ, WA), with skin and tissue substitutes explicitly included.

WISeR introduces enhanced clinical review,prior authorization or pre-payment review, earlier in the claims process. CMS is clear: WISeR does not change coverage or payment policy; it changes how rigorously medical necessity is evaluated before payment.

Translation: LCD or no LCD, utilization oversight is accelerating.

What’s Likely Next in Payment and Coverage Policy

1) The payment cap will evolve not disappear

Fixed payment is designed to compress extreme variation and blunt abusive incentives. CMS may

refine it over time to avoid restricting access to clinically superior products. Plausible next steps include:

- Adjusting the cap if access concerns emerge

- Introducing tiers so higher-evidence products are not treated identically to low-evidence alternatives

2) Regulatory status may become a sorting mechanism

To reduce subjectivity, CMS may increasingly look to regulatory status as a proxy for rigor, such as:

- 361 HCT/Ps

- 510(k)-cleared devices

- PMA-approved devices

- BLAs (which currently remain under ASP)

Regulatory pathway is not clinical effectiveness, but it is an administratively clean way to stratify products within a capped framework.

3) LCD revival is unlikely; an NCD path is more plausible

A near-term “LCD reboot” feels unlikely if CMS’s broader objective is national consistency. The more durable endpoint is a National Coverage Determination (NCD) over time, particularly if MAC-level variation continues to drive inconsistent utilization, spend, and enforcement outcomes.

Bottom line: the system is moving toward national standards and evidence will be the currency.

What to Expect Operationally in 2026

Expect more friction, more proof, and more review:

- Earlier and more aggressive pre-payment screening of claims

- Increased audits and less tolerance for templated documentation

- More conservative utilization behavior by facilities and IDNs

- Formulary rationalization and clearer product selection criteria

- Contracting that shifts toward outcomes, total cost, and documentation readiness

The winning posture is not hoping policy loosens, it’s building an evidence-and-documentation engine that performs under scrutiny.

Three Themes to Win in CMS’s Multi-Pronged Reset

1) Products with better clinical evidence will win

In a capped environment, the market rewards performance:

- Better healing rates, fewer applications, fewer complications

- Lower total episode cost

- Clear patient selection and consistent outcomes

Evidence becomes a competitive moat, not a marketing claim.

2) Clinical evidence and documentation are now compliance tools

Weak documentation can sink even appropriate care. Providers must clearly demonstrate:

- Medical necessity and wound progression

- Prior treatments and rationale for escalation

- Treatment plans, application details, and follow-up

- Alignment between documentation, coding, and billing

Audit-ready documentation is no longer optional.

3) As CMS moves toward national policy, data collection must start now

If coverage standardizes nationally, real-world data will matter:

- Structured outcomes, not anecdotes

- Repeatable results across sites

- Subgroup performance and appropriate-use criteria

Those who delay will be forced to backfill evidence under tighter reimbursement and heavier review.

Final Thought

CMS’s approach to the CTP market is clearly multi-pronged: payment reform, utilization management, and rising expectations around evidence and documentation. The organizations that succeed will be the ones that align clinical care, data, and compliance from the start.

At eKare, we see this shift daily. Providers don’t just need better products, they need better clinical documentation, defensible evidence, and scalable ways to support trials, audits, and outcomes measurement. Those capabilities won’t just support compliance; they will define who leads in the next era of wound care. The era ahead belongs to measurable outcomes, disciplined utilization, and audit-ready care.

References:

About Patrick Cheng

Patrick Cheng is co-founder and CEO of eKare, Inc. Before starting eKare, Patrick was Technology Commercialization Officer at the Sheikh Zayed Institute (SZI) for Pediatric Surgical Innovation. Prior to that, he conducted R&D in the field of minimally invasive and image‐guide surgery. Patrick received MBA from Georgetown University, MS in Biomedical Engineering with focus on medical imaging and image analysis from the University of Iowa, and BS in Biomedical Engineering from Shanghai Jiao Tong University.

Patrick Cheng is co-founder and CEO of eKare, Inc. Before starting eKare, Patrick was Technology Commercialization Officer at the Sheikh Zayed Institute (SZI) for Pediatric Surgical Innovation. Prior to that, he conducted R&D in the field of minimally invasive and image‐guide surgery. Patrick received MBA from Georgetown University, MS in Biomedical Engineering with focus on medical imaging and image analysis from the University of Iowa, and BS in Biomedical Engineering from Shanghai Jiao Tong University.